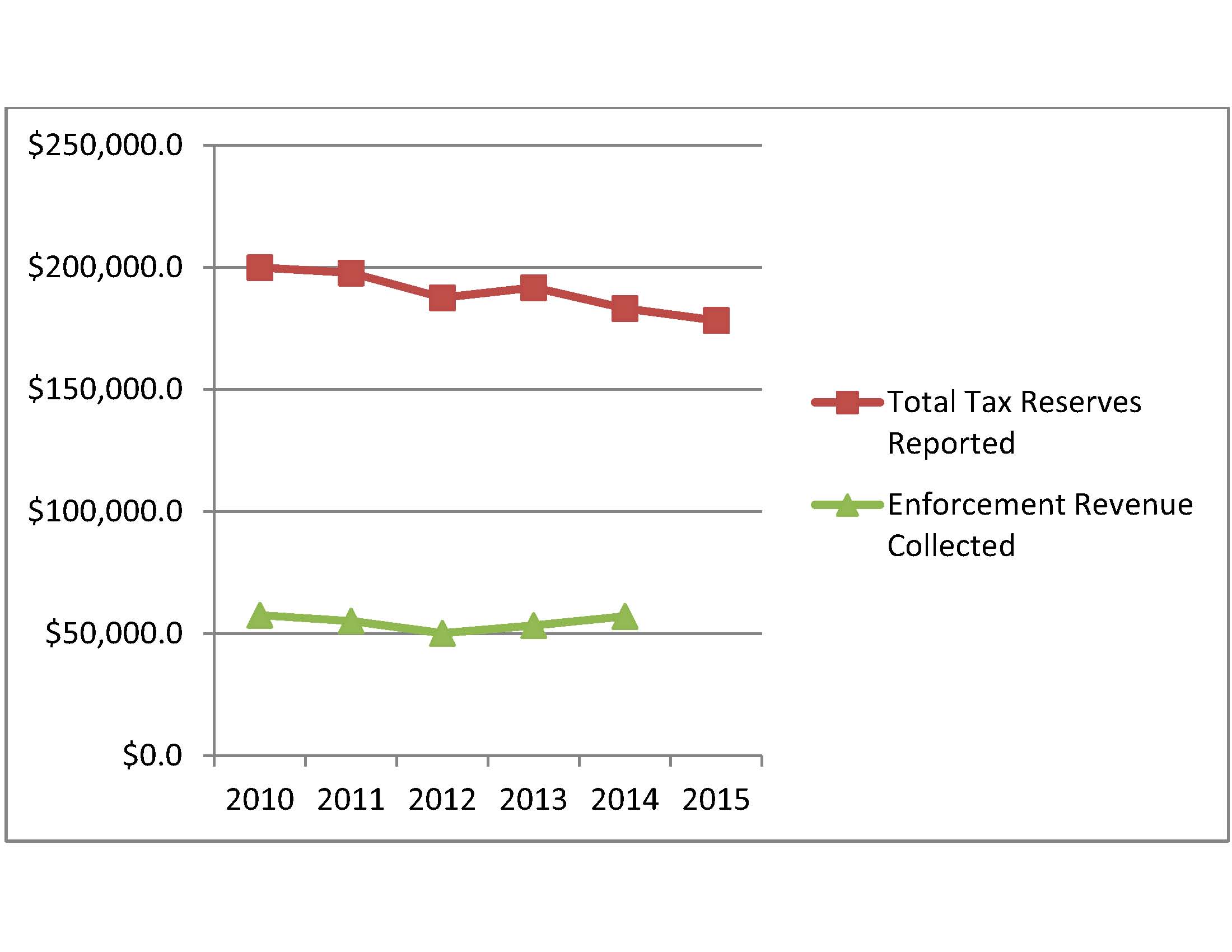

We began reordering the Fortune 500 based on uncertain tax positions reported in the most recent 10-K filed before June 15th of that year in 2010, the same year that the IRS announced that it was planning to require that certain business taxpayers to report uncertain tax positions on their tax returns. The IRS implemented a five-year phase in of Schedule UTP, requiring corporations that have total assets of $100 million or more to file Schedule UTP beginning with the 2010 tax year. The total asset threshold for the filing requirement dropped to $50 million for the 2012 tax year and to $10 million for the 2014 tax year. At the same time that corporations were expected to begin disclosing their uncertain tax positions the IRS’s budget started to be cut, year after year. According to the Center on Budget and Policy Priorities, the IRS’s budget has been cut by 18 percent since 2010, after adjusting for inflation. The IRS’s budget constraints have cut into enforcement efforts, but this should not be reflected in the uncertain tax positions reported because the likelihood of an audit on the issue is not a factor when setting the reserve. The total amount collected by the IRS through enforcement actions has remained in the $50 billion range for Federal fiscal years 2010 through 2014.*

We had assumed that tax reserves would decrease because corporations would not want to report their uncertain tax positions to the government. This assumption seemed reasonable given the amount of concern and interest in the topic by practitioners. However, the total cumulative uncertain tax positions of the Fortune 500 has been reasonably stable, even increasing on the 2013 Ferraro 500. Using the 2010 Ferraro 500 as the base line measurement for pre-Schedule UTP reserves, as this data reflects uncertain tax positions that were reported in 10-Ks published prior June 15, 2010. As a whole the Fortune 500 has only reduced its tax reserves by 10.8 percent over the last five years.

The 2015 Ferraro 500 can be found here.

* The numbers is the chart are for the Federal government’s fiscal year, October 1 through September 30. Enforcement revenue collected in a fiscal year includes tax, interest, and penalties from multiple years.

Recent Comments